In a multi-family office vs financial advisor comparison, the core difference is coordination. A traditional financial advisor usually manages one slice of your financial life — often the investment portfolio. A multi-family office (MFO) coordinates the whole picture: tax strategy, investments, insurance, retirement income, and estate planning, all under one fiduciary-led plan. For a business owner, that integration is where real wealth is often kept or lost.

What is a multi-family office?

A single-family office is a private team that manages the entire financial life of one very wealthy family. It is expensive, and historically it has been reserved for families with $50 million or more. A multi-family office takes that same coordinated model and serves several families at once, which makes the structure available to more business owners.

The point is not just more services. It is one team that sees everything and makes the parts work together.

- Multi-family office (MFO)

- A firm that coordinates investments, tax strategy, insurance, retirement, and estate planning for multiple families under one relationship.

- Family office for business owners

- The same coordinated model adapted for owners whose business and personal finances are tightly linked.

- Integrating layer

- A role that sits above your CPA, attorney, and other professionals to make sure their work aligns inside one strategy.

An MFO is not another advisor in your orbit. It is the team that finally connects the advisors you already have.

What does a multi-family office do differently than a financial advisor?

Most business owners do not have one financial life. They have several disconnected ones. A CPA files the taxes. An advisor manages the investments. An insurance agent sold a policy years ago. An attorney drafted a trust. None of them talk to each other, so the owner becomes the middleman — the only person who sees the whole picture.

A multi-family office is built to remove that burden. Here is how the two models compare.

| Area | Traditional financial advisor | Multi-family office |

|---|---|---|

| Primary focus | Investment portfolio | Entire financial picture |

| Tax strategy | Often outside their scope | Proactive, coordinated with your CPA |

| Coordination | Works in a silo | Integrates all disciplines |

| Standard of care | May operate under Reg BI | Fiduciary under the Investment Advisers Act |

| Estate and legacy | Referral, if at all | Part of the same plan |

| Who is the hub? | You are | The MFO is |

The difference is not that an MFO does each task better in isolation. A specialist may match any single piece. The difference is that the MFO owns the seams — the places where your tax plan fights your income plan, or your estate plan fights your investments. Those seams are where wealth quietly leaks.

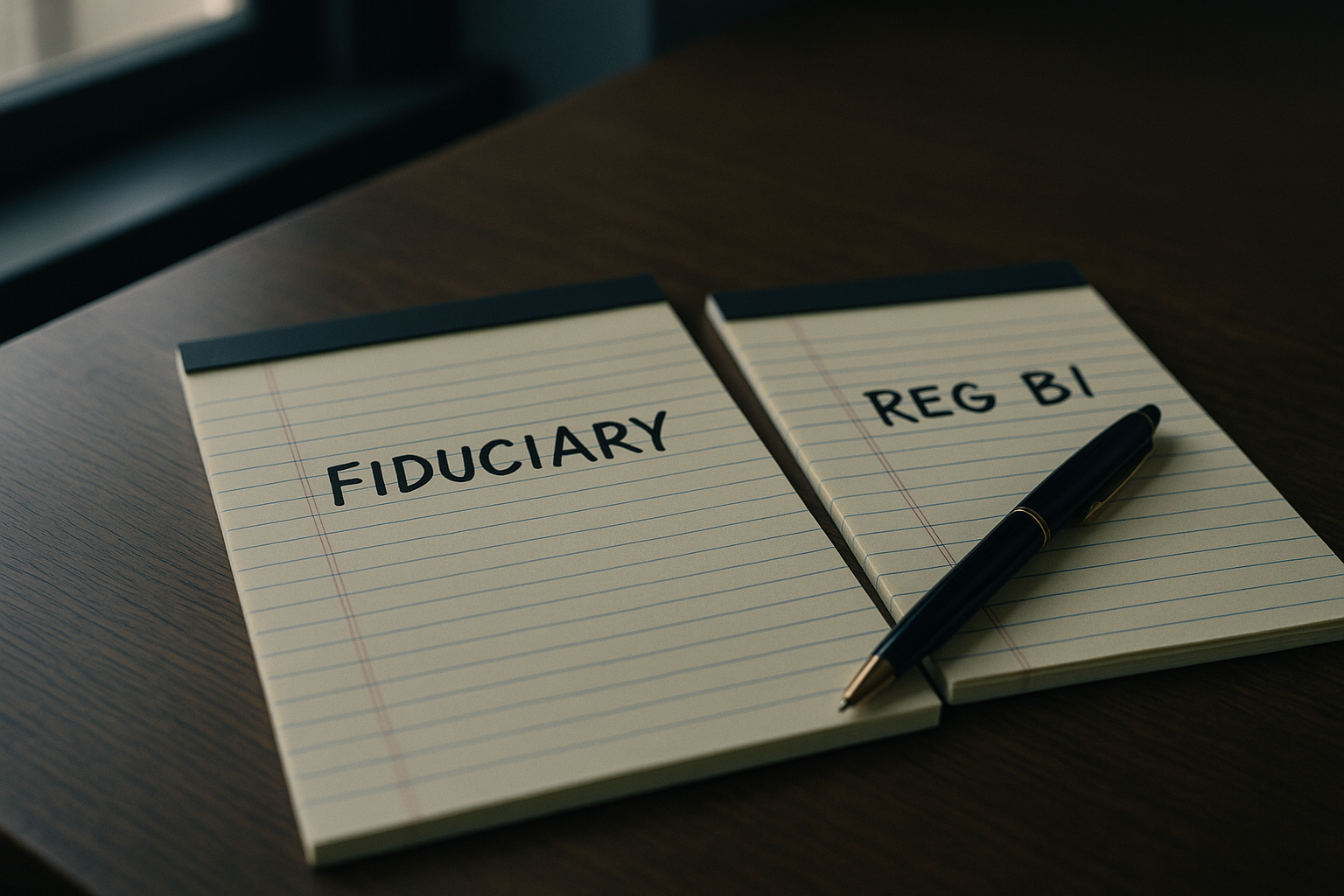

The fiduciary distinction matters

Many advisors at large firms operate under the best interest obligation under Reg BI. That is a real standard, but it is different from the fiduciary standard under the Investment Advisers Act. A fiduciary is legally obligated to act in your best interest in the advisory relationship. If you are choosing between models, ask directly which standard applies to your relationship — and get the answer in writing.

You are past the point of retail banking but below the family office threshold. That gap is where wealth can quietly erode.

Why do business owners need a family office model?

A business owner's personal and business finances are deeply linked. Your entity structure affects your taxes. Your taxes affect your retirement savings. A future business sale affects your estate. When these are managed separately, decisions in one area create problems in another that nobody catches until it is expensive.

Common gaps that surface for owners include:

- Overpaying in taxes because the CPA files but never plans ahead.

- Reaching retirement with significant assets but no clear income strategy.

- A business sale that triggers a large, preventable tax event.

- An estate plan or trust that does not function as intended when it is needed.

- A spouse who does not fully understand the financial picture.

These are not investment problems. They are coordination problems. That is exactly what the MFO model is designed to address. The tax burden on IRA and 401(k) withdrawals, for example, is something a coordinated team can plan around years in advance instead of reacting to at filing time.

How does an MFO work with my existing CPA and attorney?

This is a common worry, and the answer matters. A multi-family office does not replace your tax professional or your attorney. Your CPA still files your returns. Your attorney still drafts your legal documents. The MFO acts as the coordinating layer above them, setting direction so everyone's work points the same way.

In practice, an MFO engagement often runs like this:

- Discovery. Full visibility into all disciplines. You sign information releases so the team can see what each professional holds.

- Diagnosis. Surface gaps, overlaps, and conflicts across tax, investments, insurance, retirement, and estate.

- Coordination. One fiduciary relationship sets direction; specialists still execute inside one strategy.

- Ongoing oversight. Reviews on a regular cadence, with attention to life events like a sale, a health event, or retirement.

What does MFO wealth management cost compared to a financial advisor?

MFO wealth management is generally a relationship, not a one-time transaction. Because it covers more ground than a single-discipline advisor, the conversation is less about a single fee and more about the total value across coordination, tax planning, and risk reduction.

For a business owner, the relevant question is not only "what does this cost?" but "what is the cost of staying fragmented?" A poorly timed business sale, an unplanned tax spike, or a trust that fails under real-world conditions can dwarf any advisory fee. The MFO model is designed to reduce those avoidable costs. As with any strategy, results depend on your individual circumstances and current law.

The question is not just what coordination costs. It is what fragmentation has already cost you.

Is a multi-family office only for the ultra-wealthy?

No. That is the older model. The single-family office was built for families at the $50 million level. The multi-family office structure was created precisely to bring that coordinated experience to successful business owners and high earners who are underserved by both retail brokerages and ultra-high-net-worth family offices. If you run a business with meaningful revenue or hold significant personal assets, the coordination economics often start to make sense.

How do I know if the MFO model fits my situation?

A few signals suggest the coordinated model could be a fit:

- You work with three or more professionals who do not communicate with each other.

- You feel like you are the only one who sees your whole financial picture.

- You are approaching a business exit, retirement, or another major liquidity event.

- You want one trusted relationship instead of scattered advisory relationships.

If those describe you, the next step is a conversation — not a product pitch. The goal is to map where your current setup has gaps and whether a coordinated fiduciary strategy would close them.

Frequently asked questions

What is the difference between a multi-family office and a financial advisor?

A financial advisor usually manages one area, most often investments. A multi-family office coordinates tax, investments, insurance, retirement, and estate planning together under one fiduciary-led relationship. The core difference is integration across all five disciplines.

Does a multi-family office replace my CPA and attorney?

No. Your CPA still files your taxes and your attorney still drafts your legal documents. The MFO acts as a coordinating layer above them, making sure their work aligns inside one strategy rather than working in silos.

Is a multi-family office only for families worth $50 million or more?

No. The single-family office was built for that level. The multi-family office model was designed to bring coordinated planning to business owners and high earners who fall in the gap between retail brokerages and ultra-high-net-worth family offices.

What does fiduciary mean in this context?

A fiduciary under the Investment Advisers Act is legally obligated to act in your best interest within the advisory relationship. This is a higher standard than the best interest obligation under Reg BI that many brokerage advisors operate under. Ask which standard applies to your relationship.

How does an MFO help with a business sale?

A coordinated team can plan for the tax and estate impact of a sale years in advance, rather than reacting after the deal closes. Strategies are designed to reduce avoidable tax drag, but results depend on your business structure, sale terms, and current law.

Sources

- SEC guidance on the standard of conduct for investment advisers — supports the fiduciary standard under the Investment Advisers Act.

- SEC Regulation Best Interest (Reg BI) — supports the description of the broker-dealer best interest obligation.

- Investor.gov: Investment Advisers — supports definitions of advisory relationships and standards of care.

- IRS Small Business and Self-Employed Tax Center — supports general references to business owner tax planning and compliance.

This article is for educational purposes only and does not constitute financial, tax, or legal advice. Anchor Financial Group is a registered investment adviser; investing involves risk, including the possible loss of principal, and past performance does not guarantee future results. Consult a qualified advisor about your specific situation.